Key Takeaways:

- Private Equity Dominance: Almost three-quarter of EdTech acquisitions are now driven by Wall Street investment firms.

- Micro-Acquisition Strategy: Investors prioritize buying smaller, agile companies to mitigate risks from evolving AI technology.

- Strategic Consolidation Thesis: PE firms combine specialized tools to offer integrated platforms emphasizing simplicity and scale.

If you’ve felt like the EdTech landscape is becoming more crowded yet more consolidated at the same time, you aren’t imagining things. We are currently witnessing a fundamental shift in how educational technology is funded, built, and sold.

For years, the narrative was about “disruption” from scrappy startups. Today, the story is increasingly written by private equity firms. These changes don’t stay in the boardroom. They eventually show up on your campus, reshaping the roadmaps you rely on, the support you receive, and what you’re actually paying at the end of the day. To understand where we are headed, we have to look at the intersection of Wall Street’s capital and your campus’s digital ecosystem.

The New Drivers of EdTech M&A

I recently read a compelling report (US Education Investment Landscape: 2026 M&A Trends and Analysis) from LEK Consulting, and I’ve extracted some of those insights below and added what we are seeing in ListEdTech data.

The market itself is heating up again, growing at roughly 7% annually. But what is more interesting than the growth is who is driving it. Today, nearly half of all acquisitions are coming from private equity firms rather than traditional EdTech vendors. Recent deals like Bain Capital acquiring PowerSchool and Vista Equity Partners acquiring Pluralsight highlight just how significant this shift has become.

Corporate Acquisitions Sample (Calendar Year 2024)

| YEAR | ACQUIRER | ACQUIRED COMPANY |

|---|---|---|

| 2024 | Academic Partnerships | John Wiley & Sons |

| 2024 | Apax Partners | Zellis |

| 2024 | Arctic Wolf | Cylance |

| 2024 | Asure Software | PeopleStrategy |

| 2024 | Bain Capital | PowerSchool |

| 2024 | BMC Software | Netreo |

| 2024 | CVC Capital Partners | Epicor Software |

| 2024 | Ellucian | EduNav |

| 2024 | EQT | PageUp |

| 2024 | Follett School Solutions | LivingTree |

| 2024 | Follett School Solutions | MasterLibrary LLC |

| 2024 | Instructure | Scribbles Software |

| 2024 | KKR & Co Inc | Instructure |

| 2024 | Kohlberg Kravis Roberts | Agiloft |

| 2024 | Pathify | Navengage, Inc. |

| 2024 | Permira | Squarespace |

| 2024 | Procare Software LLC | Roper Technologies |

| 2024 | PSG Equity | Element451 |

| 2024 | SchoolStatus | SchoolNow |

| 2024 | Securly Inc. | Edficiency, LLC |

Investors are Shifting to “Micro-Acquisitions”

Private equity is playing a different game. Instead of making large, concentrated bets on established platforms, investors are increasingly looking at a fragmented market full of smaller, specialized companies.

Part of this is driven by macro conditions. Higher interest rates make large deals harder to justify. There is also a more structural concern: with AI evolving so quickly, the risk of backing a large incumbent that could be disrupted is higher than ever. Why commit billions to a single platform when you can spread that risk across dozens of smaller, more agile players?

The Challenge of “Tool Sprawl” and the Consolidation Thesis

In the short term, this leads to an obvious outcome: more tools, more vendors, and more competition. But institutions are already feeling the downside. Tool sprawl has become a real operational challenge. There are too many systems to manage, too many vendors to negotiate with, and an ever-increasing total cost of ownership.

This is where the private equity thesis becomes clearer. By acquiring and combining smaller companies (often under the $200M range), they can build more integrated platforms and sell something the market increasingly values: simplicity, security, and scale.

AI: The Great Pricing Multiplier

At the same time, AI is accelerating everything. Nearly every product roadmap now includes some form of embedded AI or copilots, not just as a feature, but as a way to deliver more value while helping justify premium pricing. For investors, that combination of higher perceived value and operational efficiency makes these “roll-up” strategies even more attractive.

A Decade in the Making: The Invisible Hand of PE

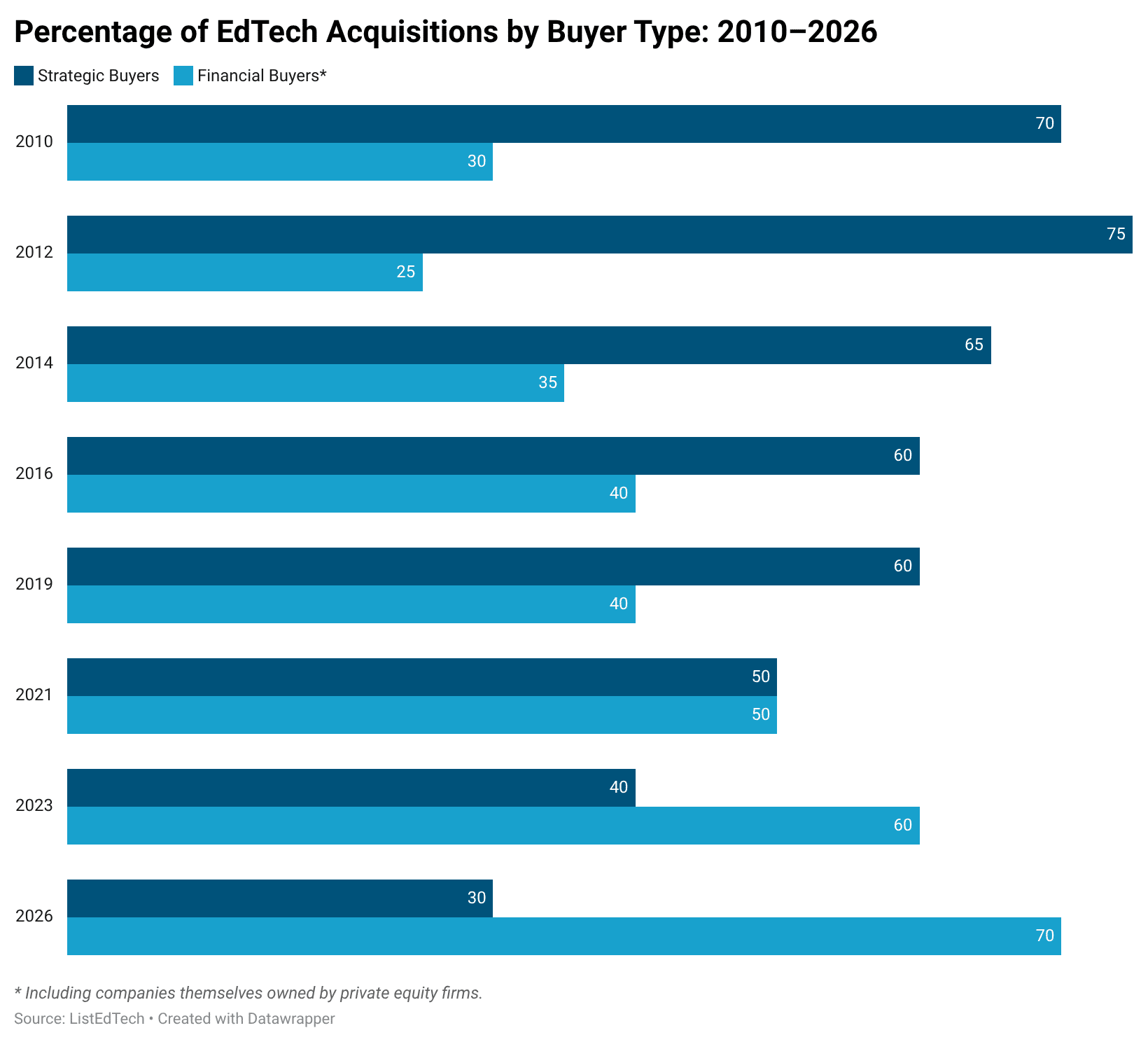

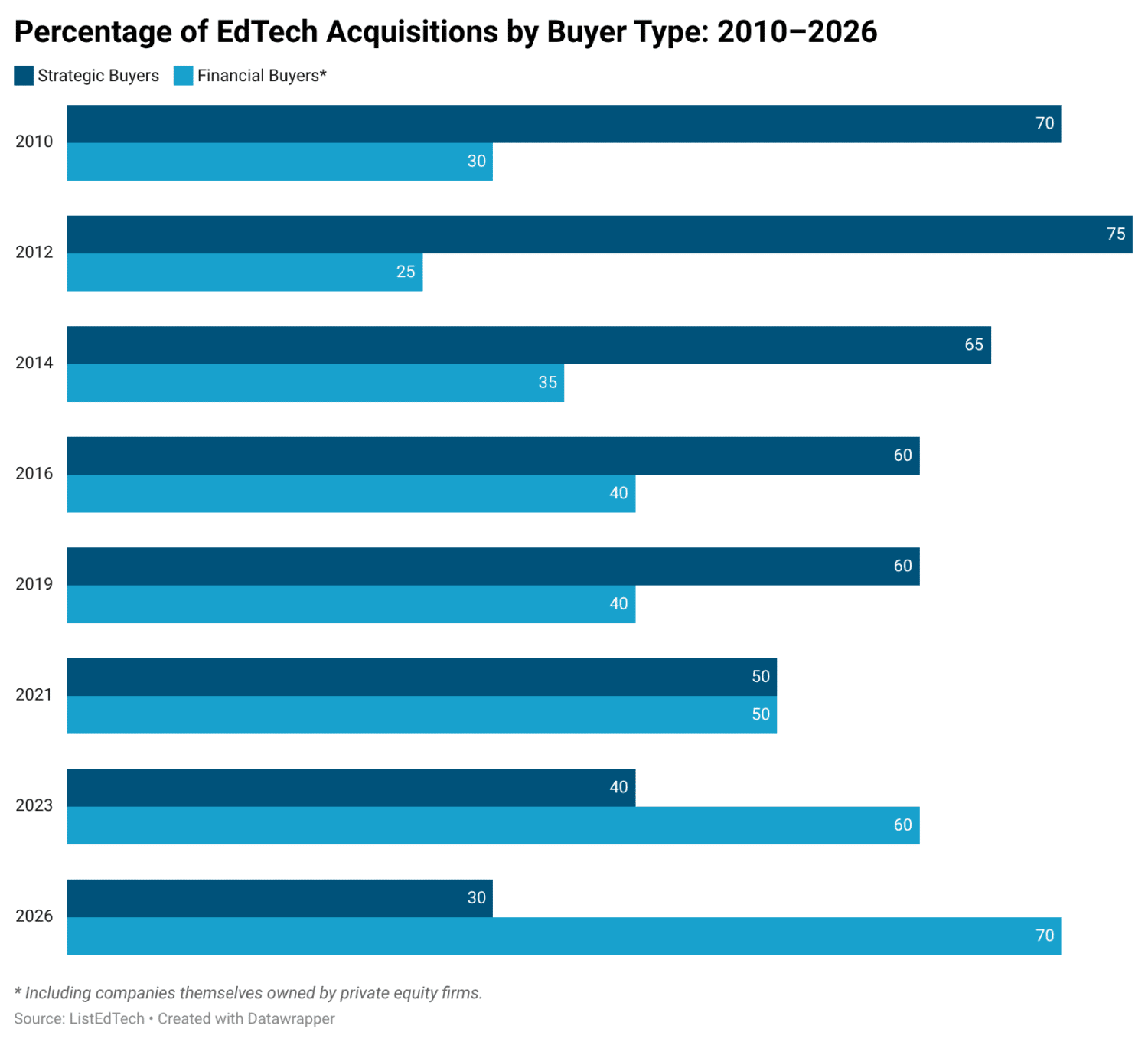

One point worth pushing on slightly: the conclusion that private equity has only recently become dominant in EdTech M&A is directionally correct, but it may understate how long this shift has actually been underway.

When we look at acquisition data over a longer time horizon, a different picture emerges. Even before the pandemic, financial buyers were already highly active. By 2015, they represented roughly 45% of acquisitions. In 2019, that number was still close to 40%, and by 2021, financial buyers briefly became the majority.

Strategic vs. Financial: A Blurring Line

Many of the so-called “strategic” buyers today are themselves owned by private equity firms. Companies like PowerSchool, Instructure, and Ellucian are often categorized as strategic acquirers. In practice, their acquisition strategies are heavily shaped by their financial sponsors.

Which means the real shift is not just that private equity is more active, it is that private equity is increasingly behind the majority of acquisition activity, either directly or indirectly. From that perspective, this trend did not start in 2021 or 2022; it has been building for over a decade.

The Future Isn’t Written Yet: Why Investment Data Isn’t Destiny

All of this points to a market entering a new phase. In the near term, we should expect continued fragmentation and a surge of well-funded tools. But over time, the gravitational pull toward consolidation and platforms will likely take over once again.

At ListEdTech, we will be watching this through a slightly different lens. Because while investment trends tell you where money is going, implementation data tells you what is actually sticking… and those are not always the same story.